SMEs account for over 90% of all businesses across the GCC. However, most of the finance teams are still managing their finances across several disconnected tools. They keep on devoting long hours every year to manual reconciliation, delayed collections, and cash flow blind spots.

DSO stretches to 45, 60, or even 90 days. It is the daily operational reality for hundreds of thousands of SMEs across the UAE, Saudi Arabia, Oman, Bahrain and beyond.

Integrated SME banking is the fix. Moreover, for GCC banks, it is quickly becoming the single most important differentiator in the SME segment.

What do you mean by Integrated Banking?

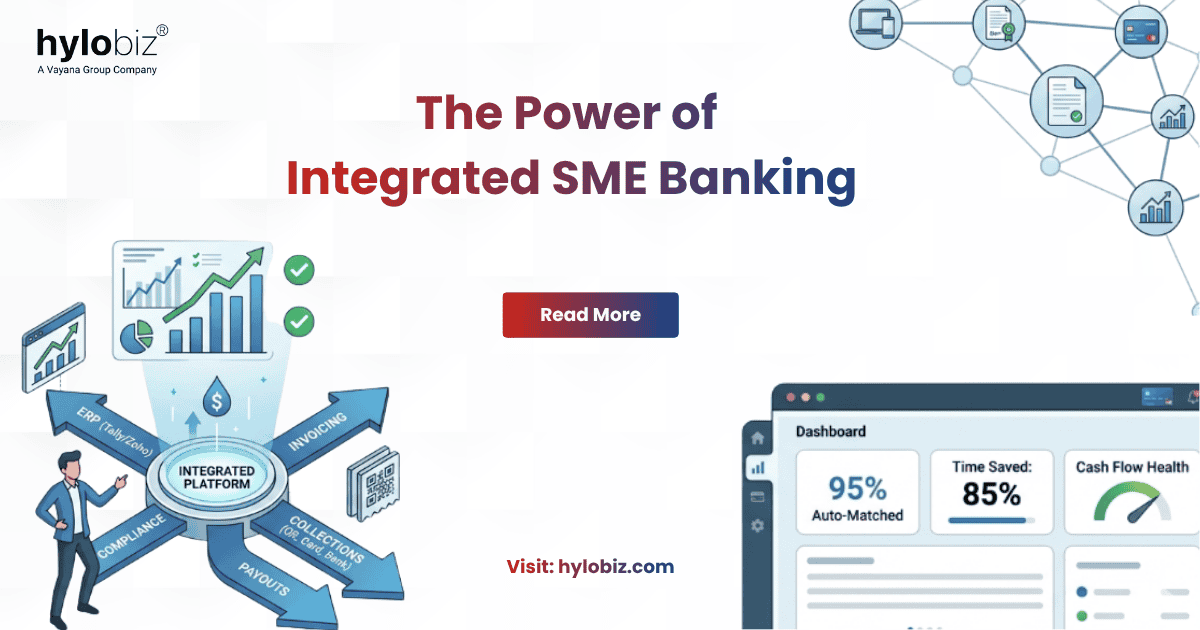

Integrated Banking is the bank account, ERP, invoicing, collections, payouts, and compliance operating as a single connected system with data flowing in real time across all of them.

Here’s how it works at the infrastructure level:

- ERP Connectivity: Secure, real-time integration with ERP platforms like Tally, Zoho, QuickBooks, and others via APIs or secure file transfers. Invoices flow in automatically. Payment confirmations flow back out.

- Omni-Channel Collections: Buyers pay via cards, virtual accounts, QR codes, direct debit, cash, or cheque. Simultaneously, every payment is reconciled automatically against the correct invoice across various channels.

- Automated Payouts: Vendor payments, payroll, and utility bills are initiated directly from the connected banking interface. Bulk uploads, multi-level approvals, and automatic ERP sync are fine as is.

- Compliance, Built In: E-invoicing, VAT compliance, audit trails, and regulatory reporting are embedded into the workflow.

How does the Integrated SME Banking Experience feel like?

Here are the four pillars of integrated SME banking:

- Invoice & Collections Automation: Invoices auto-import from ERP and are distributed to buyers instantly. Virtual accounts enable near-100% automatic reconciliation within 24 hours. Payment reminders go out via WhatsApp, SMS, and email based on rules the business sets without any manual intervention.

- Connected Payouts: Bills are auto-imported from the ERP. Vendor and employee payments are initiated directly from the banking interface. Whenever a payment is made, the ERP gets updated instantly. Everything happens in real-time.

- Real-Time Business Dashboard: Detailed visibility into collections, payouts, outstanding balances, ageing buckets, and buyer-level payment behaviour. CFOs and financial leaders can make decisions based on the current data.

- Embedded Growth Services: Working capital, trade credit insurance, and reward programs surfaced directly within the banking workflow at exactly the moment the business needs them.

What Has Integrated Banking Changed for SMEs?

To understand the impact of integrated banking on businesses, here are a few points that unveil the benefits derived by SMEs:

- Businesses using integrated collections automation consistently reduce DSO by up to 40% within the first quarter.

- The moment a payment is made, the status syncs back to the ERP. This eliminates the requirement for double entry and prevents unnecessary reconciliation lag.

- Field collections, whether cash or cheque payments received outside the digital hub, can also be logged instantly, with a full audit trail maintained at the transaction level.

- The interactive dashboard gives decision-makers a view of total collections, payouts, outstanding balances and DSO tracking. CFOs can study buyer-level payment behaviour analytics and the settlement status across all channels.

Integrated SME Banking: Case Study

A Riyadh-based IT services and maintenance company with 45 corporate clients had built a strong reputation for delivery. However, at the back-office level, monthly retainers and project invoices went out reliably, but getting paid was a major issue.

Problems:

- Reminders were manual and inconsistent.

- The ERP and bank account operated in silos.

- Overdue invoices grew uncertainly.

- Collection gaps strained client relationships.

- DSO averaged 44 days.

- The finance team spent significant time regularly chasing overdue payments.

- Cash flow uncertainty persisted.

Solution:

Integrating their ERP with their bank’s connected collections platform changed the operating rhythm completely.

Impact:

- Invoices were synced and distributed automatically.

- Reminders ran on configured schedules across WhatsApp, SMS, and email.

- Every payment was reconciled in real time.

- A live dashboard now showed exactly what was outstanding, overdue, and incoming.

- Manual compilation was eliminated.

By the end of the first quarter:

- DSO fell from 44 days to 24 days; a 45% reduction.

- On-time payment rate improved from 54% to 83%.

- Finance follow-up time dropped from 90 minutes/day to under 15 minutes.

- Invoice-to-ERP reconciliation lag has been eliminated from 2–3 days to real-time.

- Overdue invoices beyond 60 days reduced by 80%.

What value does Integrated Banking bring to banks?

When a bank embeds itself into an SME’s daily operations, such as invoicing, collections and payouts, switching becomes genuinely difficult. The operational dependency is real:

- Client retention improves.

- Transaction volumes rise.

- Enriched data from live invoice flows supports smarter decision-making.

- Buyer networks enable better credit assessment.

- Greater ability to cross-sell complementary products.

The Future of Integrated SME Banking Is Already Live

Fintech-powered integrated banking has bridged the gap between banks and SMEs. By connecting ERP, invoicing, collections, payouts, and compliance into a single system, banks are finally able to offer SMEs something genuinely valuable.

Across the GCC, SMEs are already experiencing integrated banking. DSO is falling. Admin hours are being recovered. Growth decisions are being made with confidence rather than crossed fingers.

For banks, the message from fintech is that their SME clients need more than a current account. They need a partner embedded in how they operate. The banks that recognise this and act on it will own the SME segment for the next decade.

The technology is here. The results are real. All that remains is the decision to move. Hylobiz makes integrated SME banking possible; white-label, API-first, and live across the UAE, Oman, and KSA. Get in touch with our team to see how we can help your bank go beyond banking.

Frequently Asked Questions

What is Integrated Banking?

Integrated Banking is the secure, real-time synchronization of an SME’s bank account with their crucial business tools (ERP like Tally or Zoho, invoicing, compliance).

How does integrated banking benefit GCC SMEs?

Integrated banking addresses the GCC pain point of siloed financial systems, allowing SMEs to eliminate manual reconciliation, accelerate collections, gain total cash flow visibility, and ensure seamless e-invoicing and VAT compliance.

How can a bank-fintech partnership, like one powered by Hylobiz, help a GCC bank win the SME segment?

A bank-fintech partnership enables GCC banks to rapidly deploy a complete digital and integrated banking experience. By embedding itself into an SME’s daily workflow via a white-label, API-first platform, the bank achieves significant client retention, increases transaction volumes, and gains enriched data from live trade flows for smarter credit assessment.

How integrated collections automation impacts a company’s DSO (Days Sales Outstanding)?

A Riyadh-based IT services company was struggling with manual reminders and a 44-day average DSO. After integrating their ERP with their bank’s connected collections platform, their DSO fell to 24 days within the first quarter—a 45% reduction—and their overdue invoices (beyond 60 days) were reduced by 80%.

How does Integrated Banking address the challenges of multi-channel collections for SMEs?

Whether a customer pays via cards, unique Virtual Accounts, QR codes, direct debit, or physical cheque, the platform automatically reconciles every payment against the correct invoice in the SME’s ERP via integrated banking. This eliminates the reconciliation lag and ensures the ledger is always audit-ready.