Connected banking is the real-time integration of a business’s banking infrastructure with its operational systems – ERP, invoicing, collections, payouts, and compliance into one unified, intelligent ecosystem. When a business raises an invoice, the bank knows.

When a payment is received, the ERP updates instantly, automatically, without anyone touching a keyboard. When a buyer is overdue, a reminder fires across WhatsApp, SMS, and email without a single manual step.

That is the power of connected banking.

Why Connected Banking is the Need of the Hour?

Not only banks, but the majority of SMEs and Corporates operating in the GCC are struggling with disconnected systems, financial and regulatory complexities, operational costs and poor cash visibility.

Corporates:

- Reconciliation, payment chasing, and manual ERP updates.

- Stretched DSOs.

- Delay in cash visibility.

- Outstanding receivables and trapped working capital.

SMEs:

- Manage invoicing, collections, payouts, and banking across separate, disconnected tools.

- Slow access to working capital involves heavy documentation.

- No real-time view of financial health.

- Compliance complexities across GCC countries that disconnected systems cannot handle.

Banks:

- Current accounts generate minimal engagement.

- Limited visibility into how their clients run their businesses.

- Blunt credit assessment, shallow cross-selling of products.

- Poor customer relations result in less retention.

The GCC is actively demanding connected banking because the embedded finance market is projected to grow 45% by 2030 and is currently valued at $10 billion. Let’s make a note here that, there are certain forces simultaneously converging in:

- Regulatory momentum: Vision 2030 in KSA, the UAE’s Financial Infrastructure Transformation Programme, and open banking frameworks in Bahrain and Saudi Arabia are all pushing financial institutions toward deeper integration and innovation.

- E-invoicing mandates: ZATCA’s phased rollout in KSA, the UAE FTA’s 2026 mandate, and Oman’s pilot programme are creating immediate, non-negotiable demand for ERP-to-bank connectivity at scale.

- A vast, underserved SME base: SMEs represent over 90% of businesses across the GCC — yet the majority still lack access to the integrated financial tools that connected banking makes possible.

- Fintech acceleration: The UAE hosts 329+ active fintechs, and KSA has 224+ as of 2024. The ecosystem has the technology. What it needs now is for banks to deploy it at scale.

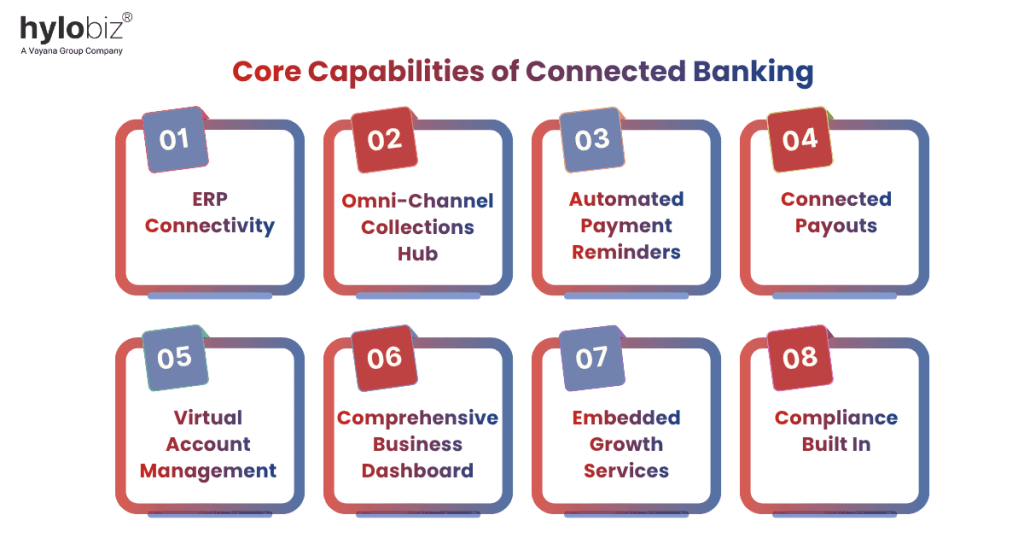

Understanding the Core Capabilities of Connected Banking

Each of the following core capabilities solves a specific gap in the current banking and business operating model:

- ERP Connectivity: Real-time integration with ERPs, with automated invoices flowing out and payment confirmations flowing back in.

- Omni-Channel Collections Hub: Accept payments across all channels online/offline – via cards, virtual accounts, QR codes, direct debit, cash, and cheque. Reconciliation against invoices across each channel is automated.

- Automated Payment Reminders: Businesses have the liberty to schedule their payment reminders and deliver them simultaneously via WhatsApp, SMS, and Email.

- Connected Payouts: Vendor payments, payroll, and utility bills initiated directly from the banking interface with multi-level approvals and automatic ERP reverse sync.

- Virtual Account Management: Unique virtual accounts per buyer or invoice enable near-100% reconciliation accuracy within 24 hours.

- Comprehensive Business Dashboard: Live view of collections, payouts, DSO, ageing buckets, and buyer payment behaviour in real-time.

- Embedded Growth Services: Working capital financing, trade credit insurance, and reward programs surfaced contextually within the banking workflow.

- Compliance Built In: E-invoicing, VAT compliance, and audit trails embedded directly into the workflow.

What are the potential advantages drawn by SMEs, Corporates and Banks from Connected Banking?

SMEs, corporates and banks are known to stay at an advantage with connected banking at its core:

SMEs:

- Enterprise-grade financial tools become accessible without enterprise-level IT investment.

- Invoicing, collections, payouts, and compliance stay unified in one bank-connected interface.

- Embedded financing is available whenever needed.

- E-invoicing compliance is handled automatically.

Corporates:

- DSO reduced by up to 40% within the first quarter of deployment.

- Finance admin hours cut by up to 75%.

- Real-time cash visibility replaces delayed, incomplete end-of-month reporting.

- Reconciliation accuracy approaching 100% through virtual account automation.

- Working capital unlocked from previously trapped receivables.

Banks:

- Better client relationships with improved retention rates.

- Increased credit assessment and cross-selling opportunities because of real-time data.

- New revenue streams from embedded finance, working capital products, and transaction fees.

- White-label deployment under the bank’s own brand.

What is the difference between Traditional Banking and Connected Banking?

The table below gives a vivid comparison between Traditional and Connected Banking:

| Dimension | Traditional Banking | Connected Banking |

| ERP Integration | None | Real-time |

| Collections | Manual follow-up | Fully automated |

| Reconciliation | End-of-month, manual | Real-time, automatic |

| Cash Visibility | Delayed by weeks/months | Live dashboard |

| Payouts | Separate process | Integrated, ERP-synced |

| Compliance | External, manual | Built into the workflow |

| Working Capital | Takes weeks, document-heavy | Instantly, Real-time |

| Client Stickiness | Low | High |

Don’t Miss Your Chance to Own the SME and Corporate Segments Now

You simply don’t have to wait for tomorrow or even later because connected banking is available and deployable now. All you need to do is deliver real value to your partners and enterprise customers.

For corporates and SMEs, it means reclaiming the time, cash flow, and visibility that fragmented systems steal every single day. Banks that embed themselves into their clients’ daily operations grow stronger connections than ever.

Hylobiz makes connected banking possible — white-label, API-first, and live across the UAE, KSA, Oman, and India. Get in touch with our team to see how we can help your bank and business go beyond banking.

FAQs

How does connected banking work?

Connected banking works by establishing a real-time, API-driven link between a business’s core accounting ERP and its corporate bank account. This allows outgoing invoices and incoming customer payments to flow seamlessly without requiring manual data entry or separate banking portal logins.

Is connected banking safe for businesses?

Yes, connected banking is exceptionally secure for SMEs, corporates, and Banks. Platforms like Hylobiz are built as high-security, institutional-grade fintech layers that comply with regulatory open banking frameworks and Central Bank standards across the GCC.

Which industries can benefit from connected banking?

Industries like Distributors, Wholesalers, Manufacturing enterprises, Logistics providers, and Professional Service firms can majorly benefit from connected banking facilities.

Does Connected Banking work with existing bank accounts?

Yes. Connected banking operates on a “Zero Process Change” philosophy designed to integrate directly with the existing corporate banking relationships. It does not require businesses to open a new account or change banks; instead, it functions as a smart, white-labeled overlay that adds automated receivables, ERP-syncing, and real-time ledger matching directly on top of the current business bank accounts.

Can businesses automate reconciliation with Connected Banking?

Yes, businesses can completely automate their reconciliation workflows. Because your invoicing ledger is tied directly to real-time cash balances, the platform uses automated Master Match engines and unique virtual accounts per buyer to instantly identify incoming transfers. This automatically settles outstanding balances and reverse-syncs data into your ERP in seconds, boasting an auto-reconciliation accuracy rate of up to 95%.